Oscillating Mkts: Blue Owl, Citrini AI 2028, $2B a week...

3 different signals, 1 big problem

🤢Capital has a bad week

Three seemingly distinct signals:

- Rising anxiety around Blue Owl and private credit,

- JPMorgan’s opaque $2B-per-week investment push, and

- The tech selloff triggered by AI crash predictions —

...are best understood as expressions of the same structural tension within the capital system.

🦉The Week’s Headlines: What Happened?

1. Blue Owl / Private Credit Stress Signals

Recent coverage highlighted investor concerns around liquidity, credit exposure, and structured private credit vehicles — particularly as software-sector repricing and broader economic uncertainty ripple into private markets.

- Business Insider – Private Credit Pressure and Blue Owl Developments

- Barron’s – Alternative Managers, Software Valuations, and AI-Linked Credit Exposure

- Swiss Re Institute – Insured Catastrophe Losses Exceeding $100B Annually

2. JPMorgan’s $2B-Per-Week Investment Strategy

Jamie Dimon signaled a major ongoing capital deployment strategy aimed at maintaining competitive advantage, while offering limited disclosure on allocation specifics — raising governance and transparency questions.

- Financial Times – JPMorgan Strategy and Shareholder Reaction

- JPMorgan Investor Relations – Primary Source Materials

3. Tech Selloff Linked to AI Crash Scenario

A widely circulated scenario outlining AI-driven unemployment and systemic market stress contributed to volatility in AI-exposed equities.

- Citrini Research – “2028 Global Intelligence Crisis” Scenario

- Federal Reserve – Distributional Financial Accounts (Wealth Concentration Data)

- U.S. Treasury – Federal Revenue Composition (Wage-Tax Context)

🧵The Common Thread

At first glance this looks like investors reacting to rising volatility in private credit portfolios, shareholders having discomfort with large undisclosed strategic spending, and sharp repricing of AI-exposed equities. Zoom in and you'll see a common thread: capital concentration at a rarified upper percentile of the economy, but scarcity at the operating layer of the economy.

Private Credit's honeymoon is over

As banks tightened lending standards in the wake of the Global Financial Crisis, Private Credit expanded rapidly, filling a funding gap with yield-seeking capital. Investors (pension funds, endowments, sovereign wealth, insurers, family offices, etc) saw private credit as a source of higher yields, but these investments carry risks that become more pronounced during economic stress.

That growth occurred alongside rising climate-related insurance losses, tighter retrocession capacity, and increasing regulatory scrutiny of non-bank financial institutions. As reinsurers retreat and capital reserve requirements rise, alternative asset managers absorb more volatility. The prevailing narrative — that private credit is more flexible and safer than traditional banking — is now being tested by liquidity mismatches and layered risk structures. In an environment of high government debt, persistent inflation, and wealth concentrated among the top 1–3%, capital remains plentiful, but the risk it carries is becoming more opaque.

JPMorgan’s spending posture reflects a related dynamic

With strong capital levels but softer loan demand amid higher rates, the growth engine is moving from traditional lending toward technology, data, and AI-driven competitive advantage. The tension between shareholder transparency and strategic secrecy highlights a broader governance question: when productive borrowers are harder to find, financial institutions increasingly deploy capital into defensive moat-building rather than credit expansion. Excess deposits accumulated during quantitative easing must earn returns, and if AI compresses margins or employment, the tax base that underwrites fiscal stability could weaken, amplifying systemic sensitivity.

AI has markets oscillating between two extremes

The tech selloff tied to AI crash scenarios underscores how narrative volatility now functions as a market risk factor in its own right. Equity gains have been concentrated in mega-cap technology firms, making valuations highly sensitive to shifts in earnings assumptions.

If - as foretold in the now famous Citrini post - AI materially disrupts mid-skill employment, the implications extend beyond equity markets: wage-dependent tax systems face pressure, deficits widen, and currency stability becomes more fragile. Markets are oscillating between two poles — AI as productivity miracle versus AI as social and fiscal shock — and that oscillation reflects a deeper feedback loop. When capital concentration increases while wage growth and policy headroom diminish, volatility becomes structural rather than episodic.

🪷a macro haiku

Ok not really a properly structured haiku...

- Climate & Insurance: Retrocession capacity tightening, Climate losses increasing capital volatility, Private credit and alternative managers absorbing displaced risk

- Fiscal Fragility: Government debt growing faster than GDP, Inflation + tariffs distort cost structures, Tax base structurally vulnerable to wage displacement

- Wealth Concentration: Top 1–3% accumulating capital, Capital chasing yield in private markets, Broader population exposed to wage instability

...but it is short and sweet.

The Ecosystem Analogy - how to think about what's going on

There are 3 related factors playing out inside the overall capital system:

- Capital owners hold an extremely high concentration of wealth

- Capital owners are reliant ultimately on wage earners (who hold a small percentage of wealth) for continued growth.

- Governments have been able to alleviate or mask this tension via subsidies and tax breaks to corporations but most governments seem to be running out of headroom for this kind of policy.

Economies are like ecosystems. In ecosystems, the circulation of water is important.

In economies, the circulation of wealth is important.

Wealth circulation happens via:

- Jobs (wages)

- Tax policy,

- Subsidies or

- Charitable donations

- Investment

When these methods fail (or are used improperly) you end up with wealth concentration.

In the US currently all 5 methods of wealth circulation are being constrained:

- Reduced subsidies (ACA and other, in part due to policy preferences and in part due to rising government debt)

- Reduced taxes (tax breaks)

- Reduced incentives for charitable donations (in an apparent attempt to curtail funds to perceived enemies)

- Reduced jobs - thanks to AI

- Investments are becoming circular - also thanks to AI

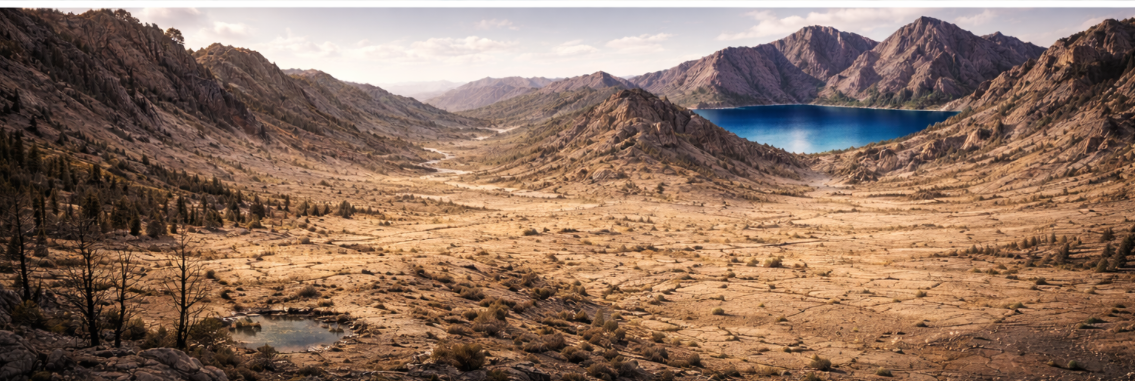

Imagine a landscape where there is one large lake and one small dwindling water hole. No streams, or rivers, no evaporation or rainfall...in other words no circulation of water.

That's a rough analogy of what happens with wealth becomes concentrated among the top 5%. It becomes harder and harder to grow that wealth. You can't expect to continue to grow the size of a large lake by draining the dwindling watering holes.

In today's economy the upper 10% is searching for a way to continue growth off the portion of the economy that has the least wealth and flat, if not declining wages.

Wealth holders may keep adding zeros to the ends of their fund amounts. But that's inflation at work, not value creation.

It all comes back to capital

This week three seemingly unrelated stories, Blue Owl, JPMorgan, tech selloff turn out to be signals of the same structural tension inside the capital system. Wealth is increasingly concentrated at the top, yet that capital ultimately depends on wage earners, borrowers, and stable policy frameworks for growth. The capital system is becoming more fragile and narrative-driven. Volatility isn't episodic any more, it's becoming structural.

So yes Capital is having a rough time. But that doesn't mean you have to. Sign up for S3T full access and learn the Signal to Skills checklist of how to position your team for success during these turbulent times.

You'll also learn how to use the Five Layers of Strategic Awareness: to look past headlines and see the underlying realities — incentives, governance, capital concentration, fiscal constraints, and narrative shifts — that actually drive outcomes. When you understand these layers, you don’t chase noise. You build strategic advantage.