S3T Jan 23: CBDC 20 Questions, Capital Protectors, Evolution of Governance, Financial Primitives, Bird Names, Irruptions and more...

As crypto and tech markets fall, inflation and employment rises, and the Fed mulls CBDCs, the evolution of governance continues with new questions about the responsibilities of capital managers, and new opportunities for leaders who want to implement change faster.

Finance

Federal Reserve CBDC Paper

The Federal Reserve has released its long awaited paper on Central Bank Digital Currencies (CBDC) titled Money and Payments: The US Dollar in the Age of Digital Transformation. In their release statement, the Fed positioned the paper as a first exploratory step, to solicit and review "a wide range of views as it continues to study whether a U.S. CBDC would be appropriate."

Pros and Cons:

- Pros: A CBDC might help preserve the international role of the dollar, boost financial inclusion, enable rapid and cost-effective delivery of wages, tax refunds,and other federal payments.

- Cons: A CBDC might cause systemic risks, put other assets at a disadvantage, be a target of hackers. The paper noted also that the government may struggle to balance privacy and data protection vs. the desire to prevent financial crimes.

Other Highlights:

- Cash use in the US is down from 40% of transactions in 2012, to 19% in 2020. The decline is more rapid in other countries.

- Central banks are researching "offline CBDC payment options" (TEE, PKI in combo with NFC, Bluetooth as described here) to enable better security, and continuity during disasters.

The release statement invites readers to share their views by answering 20 questions on this comments form.

Healthcare

Moral Hazard Part III

Caveat: The language here may seem unfair and accusatory to the passionate and deeply caring individuals working across the different industry verticals in healthcare. To be clear, we're attempting to describe the economics in play, not the intentions and character of the individuals working inside the systems guided by those economics.

Who are the "bad actors?"

As described last week, moral hazard in healthcare is described as if patients were the "bad actors", and that charging them more, or complicating their care pathways is just a necessary evil for counteracting the behaviors of these "bad actors."

It seems like such an obtuse position, in the face of the national crisis of healthcare affordability.

But for the financial establishment of healthcare it could also be very convenient line of financial logic: it justifies raising prices and taking a greater and greater share of GDP, while blaming things on "consumers."

But what do we mean by the financial establishment of healthcare?

This is where it is important to be very clear about who or what we might actually accuse:

Do not think in terms of individuals, companies or even healthcare industry segments.

Think in terms of economic roles.

There is a specific role that exists across the different verticals of healthcare:

- That role in some way is responsible to preserve and grow capital.

- This role is not evil. It has a legitimate purpose.

- This role holds profound influence over healthcare processes and outcomes.

- This role is subject to moral hazard.

Look at any government healthcare program, any hospital system, insurer, just about any team or organization in healthcare, and you will find a person or team that is required to play this role.

The Role that is subject to Moral Hazard

Let's call this role "Capital Protector", and let's define it:

A Capital Protector is an entity that has a responsibility to preserve and grow capital. The Capital Protector entity may directly own the capital, or may be managing capital entrusted to it by another entity. The Capital Protector entity could be an individual, an organization, or even a set of affiliated organizations who have a shared interest in preserving a set of capital.

What are examples of Capital Protectors at work?

- For-profit healthcare companies working to provide profits to shareholders.

- Healthcare VCs try to generate largest possible revenues and ROI for new medical devices and treatments.

- Health system finance teams trying to ensure healthy balance sheets.

- Health insurers trying to maintain required reserves.

These entities have a large set of protective instruments at their disposal. A few examples (each of these are actually categories of protective instruments):

- Political connections to ensure that rules are written in their favor.

- Insurance barriers that can be used to reduce how much is paid to cover a patient's treatment cost.

- Regulation designed to protect investors and protect capital.

So where does the moral hazard arise?

If we state what moral hazard is in simple terms...

If I am given some kind of advantage, I may be tempted to take advantage of it in an inappropriate manner.

We can restate the moral hazard premise as follows:

Moral hazard in healthcare exists when capital protectors use the large set of protective instruments at their disposal to obtain one-sided benefits for themselves at the expense of individuals who need healthcare.

To summarize

As we learned in previous posts, the conventional healthcare industry thinking on moral hazard holds the following:

- Moral hazard exists and that it is a risk to the industry

- Consumers are the cause and source of this moral hazard

- Onerous mechanisms like cost and complexity are appropriate and necessary for managing this moral hazard

It turns out that Capital Protectors are actually the source of moral hazard in healthcare. This raises the interesting question: what might be the "onerous mechanisms" appropriate and necessary for managing this moral hazard?

And is an onerous control mechanism actually what is needed? Or should it be a change in healthcare that reframes the risk/reward equation and aligns our shared interests in a more productive equitable way? And what are the responsibilities of capital managers to their societies? I want to develop this idea further in future editions.

If we want to achieve this kind of foundational change in healthcare, then what is the most timely and effective approach for doing so? The next segment on Implementation Paths starts to answer that.

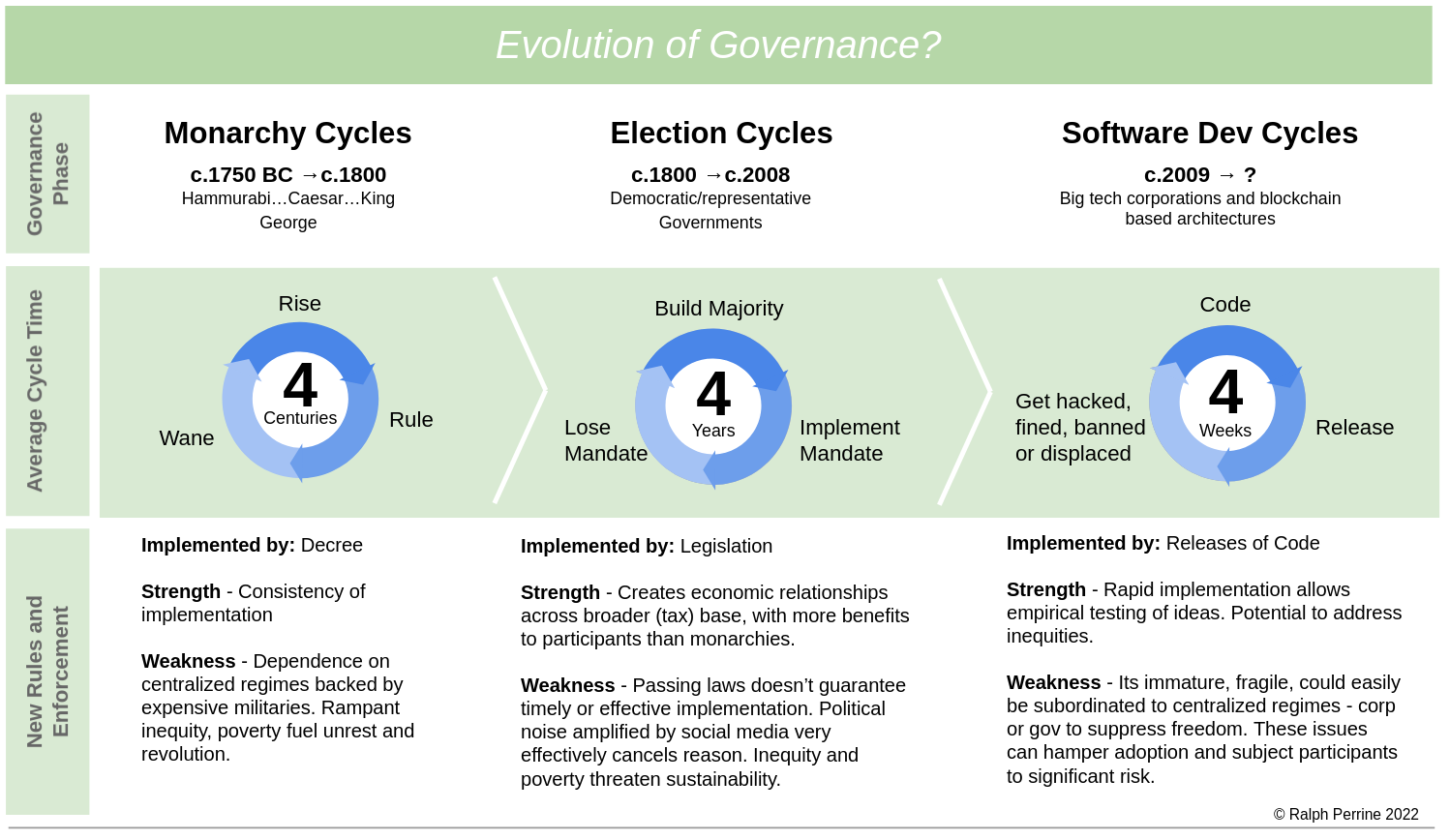

Implementation Paths and the Evolution of Governance

As change leaders, we naturally seek the fastest path rapidly solve the complex and urgent problems of our world.

Learning how to solve a complex problem requires attempts at implementing solutions, learning from the implementation attempts, and iterating or pivoting until the desired outcomes are being achieved.

Given this, it's helpful to know what implementation platforms are available and which ones allow for the most empirical learning in the least amount of time (and money).

Implementation platforms have a direct relationship with governance, and governance is evolving as shown here:

Implementation Path #1: Decree

The world's oldest implementation platform - where a king, religous leader or similar power decrees that something will be built, invaded or enforced - still has relevance today. Authoritarian governments follow this playbook when they do things like ban bitcoin mining, for example. Large transnational companies can also weld this kind of power. Limitations of this approach:

- It stems from centralized ideation that is narrowly focused on serving the needs of those in power.

- It overlooks or suppresses the needs and human rights of its dependent populations.

- You can't use this option unless you are the one with the power.

Implementation Path #2: Legislation

Typically the first thought of - implementation platforms is the law. Write policies and legislation and get it enacted into law. Once the law is passed, think tanks and universities conduct studies reviewing the impact and cost-benefits of the policy, and recommend changes (or often, further study 🙂 ).

Implementation Path #3: Software Release

Today we have a newer, faster way of implementing large solutions (and sometimes large problems): Building an releasing a platform or app - think Facebook, TikTok, Slack and think about the huge influences they have had. Emering blockchain architectures seem set to push this even further, by combining code, currency and governance into a single programmable layer.

Compare the speed of these platforms

Legislation is the slowest Implementation Path. Consider Healthcare Reform:

- FDR mulled and then abandoned a healthcare agenda,

- Eisenhower briefly floated a National Reinsurance Program,

- Hillary Clinton proposed reforms that were rejected.

- Finally the ACA implemented a set of measures that achieved notable improvements in national coverage, but continue to be debated and questioned by partisan players.

In addition to being the slowest implementation platform, legislation is also - thanks to the partisan bedlam that surrounds any meaningful change - the least likely to allow emperical learning and clear conclusions. Policy does not lead. It lags and gridlocks. Over and over lawmakers struggle to understand the changes being put in motion by technology - whether from the rise of the Internet, or more recently the rise of blockchain based ecosystems.

By contrast consider the rapid rise of transnational corporations like Facebook/Meta - and the impactful platforms and new patterns it implemented. From a small group of college students to a collective user base larger than most nations of the world, developing its own currency and demonstrating more soft power and influence than most nations of the world.

Today the emerging decentralized blockchain architectures, and the financial ecosystems being built on top of them, show indications of unleashing change in even bigger and faster ways. These architectures do not simply offer building blocks of code - the building blocks are both code and at the same time programmable financial primitives. That's why they represent an evolutionary forward step in governance.

The point is, software releases offer much faster more scalable implementation paths than legislation can. If you are serious about solving the pressing problems in your community, nation or world, your options for faster implementation are getting better all the time.

It feels "full circle" but with a twist: If you go way back, one of the earlier implementation platforms were the decreed charters that European kings granted to shipping companies. The charters granted wide powers enabling these companies to exploit the natural resources of colonized territories, provide increased tax revenues for the crown, and - where possible - interfere with or contain the colonial profit-making of other European nation-states.

The implementation platform that enabled this colonial era was primarily a financial one. The roots of our modern insurance industry derive from this era.

As we stand on the threshold of the next generation financial ecosystem it feels a little like we have come full circle.

But this time, instead of working solely for the health and wealth of a few European kings, we might - just might - have a chance to be focused on enabling a healthy wealthy world.

Watch: DAOs and Politics

As election season heats up over the course of this year, watch for political teams/ candidates experimenting with ways to leverage DAOs for fundraising.

Outdoor Notes

Bird Names

Nightjars, Shearwaters, Noddies, Loons ...Why are birds given such outlandish and odd names?

Birds of the World has embedded a new exhaustive resource on bird names, based on the life work of James Jobling.

If you love to haunt used book stores (online or in person), here is a treasure to keep an eye out for: Earnest Choate's Dictionary of American Bird Names has a similar resource featuring bird names with their meaning and origins.

Irruptions

Why is Tyler Hoar's Finch Irruption Report required reading by so many people with bird feeders in their yard?

Well, North America is home to a variety of finch species that depend on wild berries, pine or spruce cones or seeds for survival. When these food supplies vary, "irruptions" (migratory movements further south than normal) - may bring to your yard some winter birds you usually don't get to see in the lower 48. Snowy Owls are another species that can irupt further south than normal.

Thank you again for reading. Its ok to forward this to a friend. Have a great week!

Ralph

Opinions mine. Not financial advice. I may hold assets discussed.

Member discussion